Fire & Smoke Damage

Fire Damage Insurance Claims Guide: Navigating the Process Successfully

January 22, 202612 min read

S

Sage Southard· Estimating Department Manager

Sage Southard manages the estimating department at Advanced Disaster Recovery, bringing seven years of restoration-industry experience to insurance estimating and large-loss documentation. Sage holds a Bachelor's degree in Law and Justice Studies with a minor in Business Administration from Rowan University and is OSHA 10, Xactimate Level One, and FEMA certified, as well as a Haag Certified Reviewer.

7+ years experienceOSHA 10 Certified, Xactimate Level One Certified, FEMA Certified, Haag Certified ReviewerLinkedIn

Published January 22, 2026 · Updated May 27, 2026

Complete guide to filing fire damage insurance claims. Learn documentation requirements, settlement negotiation, and how to maximize your claim payment.

Immediate Steps After Fire Damage

The actions you take immediately after fire damage significantly impact your insurance claim. Following proper procedures protects both your safety and your claim's success.Safety First

Never re-enter a fire-damaged building until fire officials declare it safe. Structural damage, toxic gases, and electrical hazards create serious risks. Wait for official clearance even if damage appears minor from outside.Notify Your Insurance Company

Contact your insurance company as soon as safely possible—ideally within 24 hours of the fire. Most policies require prompt notification and may have specific reporting timelines. When you call:- Have your policy number available if accessible

- Provide basic information about the fire (date, time, address)

- Describe damage extent to the best of your knowledge

- Ask about immediate next steps and claim filing procedures

- Request information about additional living expenses if displaced

Document Everything

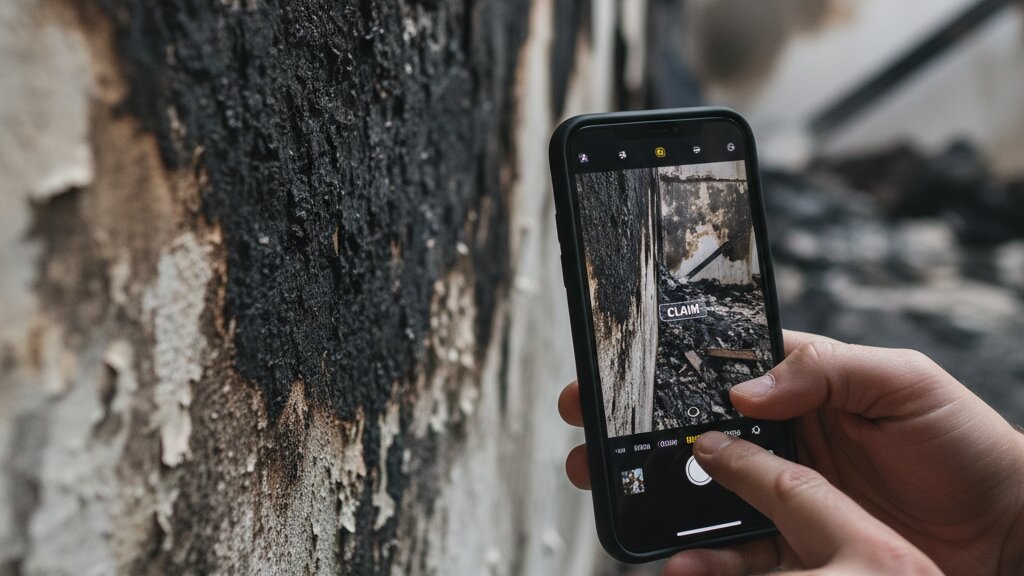

Documentation forms the foundation of successful fire damage insurance claims. Begin documenting immediately. Proper fire claim documentation protects your rights and maximizes settlement amounts: Photograph and Video: Once safe to enter, capture comprehensive visual documentation of all damage. Include wide shots of rooms, close-ups of damaged items, and exterior damage. Document smoke damage, water damage from firefighting efforts, and structural damage. Create Inventory Lists: Begin listing damaged and destroyed items with descriptions, approximate purchase dates, and estimated values. This inventory becomes critical for personal property claims. Save All Receipts: Keep receipts for all fire-related expenses including temporary housing, meals, clothing, and emergency supplies. These may be reimbursable under additional living expense coverage.

Understanding Fire Insurance Coverage

Fire damage insurance claims typically involve multiple coverage categories within homeowner or commercial property policies. Understanding these categories helps ensure you claim all entitled benefits and navigate fire damage insurance claims effectively.| Coverage Type | What It Covers | Documentation Needed |

|---|---|---|

| Dwelling/Structure | Physical damage to the building including walls, roof, flooring, built-in fixtures | Contractor estimates, damage assessments, pre-fire photos if available |

| Personal Property/Contents | Belongings damaged or destroyed including furniture, clothing, electronics, appliances | Detailed inventory lists, photos, receipts, appraisals for valuables |

| Additional Living Expenses | Costs for temporary housing, meals, and other expenses while displaced | Hotel receipts, restaurant receipts, rental agreements |

| Other Structures | Detached garages, sheds, fences affected by fire | Photos, repair estimates for each structure |

| Loss of Use (Commercial) | Lost business income during restoration period | Financial records, revenue documentation, business interruption calculations |

Actual Cash Value vs. Replacement Cost

Your policy's valuation method significantly affects fire insurance settlement amounts: Actual Cash Value (ACV): Pays the depreciated value of items—what they were worth at the time of loss, not what replacement costs. A five-year-old television might receive payment for current used value rather than new replacement cost. Replacement Cost Value (RCV): Pays to replace items with new equivalents. These policies typically pay ACV initially, then the remaining replacement cost after you actually purchase replacements and submit receipts. Review your policy to understand which valuation applies. Replacement cost coverage provides significantly better protection but may require completing replacement purchases to receive full payment. Understanding these valuation methods is crucial for fire insurance settlement negotiations.The Fire Damage Claims Process

Understanding the insurance claim process timeline and steps helps property owners navigate each phase effectively. The insurance claim process involves multiple stages from initial filing through final settlement.Claim Filing and Assignment

After initial notification, you'll formally file your claim and receive a claim number. The insurance company assigns an adjuster to your case. This adjuster investigates the claim, assesses damage, and ultimately recommends payment amounts. Proper initiation of fire damage insurance claims sets the foundation for successful outcomes. Adjuster assignment typically occurs within a few days. However, after major fire events affecting many properties, assignment may take longer due to demand. Stay in contact with your insurance company if you don't hear from an adjuster promptly.Investigation and Inspection

The insurance adjuster will inspect your property, review damage, and investigate the fire's cause. For substantial claims, insurance companies may also send:- Cause and origin investigators: Determine how and where the fire started

- Engineers: Assess structural damage and repair requirements

- Inventory specialists: Catalog and value damaged contents

Scope and Estimate Development

The adjuster develops an estimate for covered repairs and replacements. This estimate determines initial claim payment. Review this estimate carefully—adjusters sometimes miss damage or underestimate repair costs. Pro Tip: Obtain independent repair estimates from licensed contractors. If these estimates significantly exceed the adjuster's figure, you have grounds to negotiate higher payment. Restoration companies can also provide detailed scope documentation supporting higher estimates.Settlement Negotiation

Initial settlement offers aren't necessarily final. You have the right to negotiate if you believe the offer undervalues your loss. Effective fire insurance settlement negotiation requires:- Detailed documentation supporting higher values

- Independent contractor estimates

- Receipts or appraisals for valuable items

- Clear understanding of your policy coverage

Payment and Restoration

Once settlement is reached, payment processing begins. The insurance claim process for structure claims often involves multiple payments:- Initial payment: Released to begin restoration work

- Progress payments: Released as restoration reaches milestones

- Final payment: Released upon restoration completion

Working with Restoration Companies During Claims

Professional restoration companies play important roles in fire damage insurance claims beyond performing restoration work.Documentation Support

Restoration professionals provide detailed fire claim documentation that supports insurance claims:- Comprehensive damage assessments

- Photo and video documentation

- Scope of work documents

- Industry-standard pricing

- Progress documentation throughout restoration

Direct Insurance Communication

Experienced restoration companies communicate directly with insurance adjusters, explaining scope requirements and justifying necessary work. This professional-to-professional communication often resolves scope disputes more effectively than policyholder-adjuster discussions.Restoration Coordination

Restoration companies experienced with the insurance claim process understand payment timing and can often begin work while claims process. They coordinate with adjusters on scope changes and supplements when hidden damage emerges during restoration.Common Fire Insurance Claim Mistakes

Avoiding common mistakes improves fire damage insurance claims outcomes and prevents unnecessary delays or underpayment.Discarding Damaged Items Too Soon

Don't throw away fire-damaged items before the adjuster inspects them and you've documented them thoroughly. Adjusters need to see damage to approve claims. Some contents cleaning and restoration can salvage items that appear destroyed—professional assessment determines what's salvageable.Missing Damage Categories

Fire damage extends beyond obvious burned areas. Commonly overlooked damage includes:- Smoke damage in rooms distant from the fire

- Water damage from firefighting efforts

- HVAC contamination throughout the building

- Electronics damage from smoke infiltration

- Odor penetration in textiles and soft goods

- Hidden smoke damage in wall cavities and attics

Accepting First Offers Without Review

Initial settlement offers represent starting points, not necessarily fair values. Review offers against independent estimates and your documented losses before accepting. Reasonable negotiation is expected and doesn't jeopardize your claim. Thorough fire insurance settlement review ensures fair compensation.Delaying Mitigation

Insurance policies require policyholders to mitigate ongoing damage—taking reasonable steps to prevent additional loss. Delaying mitigation can result in claim denial for secondary damage. Begin professional mitigation promptly; insurance covers these costs as part of the claim. Warning: Never delay necessary mitigation waiting for adjuster inspection. Document conditions thoroughly, then proceed with mitigation. Allowing damage to worsen violates policy requirements and may result in denied coverage for preventable secondary damage.Inadequate Documentation

Insufficient documentation is the most common cause of claim disputes and underpayment. Document extensively from the beginning. More documentation always strengthens your position—you can't over-document a fire loss. Comprehensive fire claim documentation throughout every phase protects your financial interests.Maximizing Your Fire Damage Claim

Several strategies help property owners secure fair fire insurance settlement amounts reflecting their actual losses.Create Detailed Inventory

Personal property claims depend entirely on inventory documentation. For each damaged item:- Describe the item specifically (brand, model, features)

- Note approximate purchase date and price paid

- Estimate current replacement cost

- Include photos if available

- Note condition before the fire

Don't Overlook Small Items

Small items accumulate significant value. Kitchen utensils, cleaning supplies, toiletries, hobby materials, and similar everyday items warrant inclusion. These categories often total thousands of dollars when fully inventoried.Understand Depreciation Calculations

If your policy uses actual cash value, understand how depreciation is calculated. Challenge unreasonable depreciation schedules. A quality appliance properly maintained shouldn't depreciate as rapidly as cheap alternatives.Request Itemized Adjustments

When disputing settlement offers, request itemized breakdowns showing how values were calculated. This visibility reveals where disputes exist and focuses fire insurance settlement negotiation productively.Additional Living Expenses Claims

When fire damage displaces you from your home, additional living expense (ALE) coverage pays costs beyond your normal living expenses. Understanding ALE coverage helps you access these benefits appropriately.What ALE Covers

- Hotel or rental housing costs exceeding your normal housing payment

- Restaurant meals exceeding normal food costs

- Laundry expenses if facilities aren't available

- Storage fees for salvaged belongings

- Pet boarding if temporary housing doesn't allow pets

- Additional transportation costs

Documenting ALE Expenses

Save every receipt related to displacement. Track expenses daily and submit claims regularly rather than waiting until restoration completes. ALE coverage has limits and time restrictions—understand your policy's specific terms.Frequently Asked Questions About Fire Damage Insurance Claims

How long do fire damage insurance claims take to settle?

+

Settlement timelines vary based on claim complexity and insurance company responsiveness. Simple claims may settle within weeks; major losses can take months. Factors affecting timeline include investigation requirements, scope disputes, contractor availability, and documentation completeness. Understanding the insurance claim process helps manage expectations. Stay in regular contact with your adjuster to keep claims moving.

Can I choose my own restoration company or must I use one the insurance company recommends?

+

You have the right to choose your restoration contractor. Insurance companies may recommend preferred vendors but cannot require their use. Select qualified, certified professionals based on credentials and experience. Your choice doesn't affect claim coverage—insurance pays reasonable restoration costs regardless of which qualified company performs the work.

What if the insurance company's estimate is much lower than contractor quotes?

+

Significant estimate gaps are negotiable. Provide detailed contractor estimates explaining scope differences. Request meeting between your contractor and the adjuster to discuss discrepancies. Insurance companies use standardized pricing software that may not reflect local market conditions or specific repair requirements. Documented justification for higher costs typically results in adjusted fire insurance settlement amounts.

Should I make temporary repairs before the adjuster visits?

+

Make necessary temporary repairs to prevent further damage—this is required by your policy. Document conditions thoroughly before repairs and keep all receipts. Temporary mitigation like board-up services and tarping is covered and expected. Permanent repairs should wait for adjuster inspection and scope approval.

What if my claim is denied?

+

Claim denials can be appealed. Request written explanation for denial and review your policy to verify the cited exclusion applies. Many denials result from misunderstanding or incomplete information rather than legitimate coverage gaps. Submit additional documentation addressing denial reasons. If appeals fail, consider hiring a public adjuster or consulting an insurance attorney.

Does filing a fire claim affect my future insurance rates or coverage?

+

Filing claims may affect future premiums, but fire damage from covered causes shouldn't result in non-renewal for single incidents. Rate impacts vary by insurance company and claim history. Not filing legitimate claims means paying for insurance without using coverage you're entitled to. Document the claim properly and let insurance serve its intended purpose.

Professional Fire Damage Restoration and Insurance Support

Navigating fire damage insurance claims while managing restoration requires coordination and expertise. Professional restoration companies experienced with insurance processes streamline both the restoration and claims aspects of recovery. Expert support throughout fire damage insurance claims ensures maximum settlement recovery and quality restoration. When fire damage affects properties in Northern New Jersey, Pennsylvania's Capital Region, New York's Hudson Valley, Connecticut's Capital Region, or the South Jersey Shore, certified restoration professionals provide both expert restoration services and documentation support that helps property owners navigate the insurance claim process successfully.Categories

Need Restoration Services?

Our team is available 24/7 for emergency response. Call us today for a free phone consultation.

Questions About Restoration?

Our experts are ready to help. Contact us for a free consultation.